Trending Now

- 830 voters names go missing in Kavundampalayam constituency

- If BJP comes to power we shall consider bringing back electoral bonds: Nirmala Sitaraman

- Monitoring at check posts between Kerala and TN intensified as bird flu gets virulent in Kerala

Coimbatore

Global Bond Inclusion – A Win for India

![]() September 25, 2023

September 25, 2023

Introduction

10 Years to the day, India suffered one of its worst balance of payments crises leading to a sharp deterioration in its currency and labelled as a ‘Fragile Five’ nation. Fast forward to 2023, a series of gradual policy reforms have allowed India to expand its global clout in the world of market finance and further integrate into the global financial system. The announcement today by JP Morgan to include select Indian government securities into its emerging market indices is a ‘material’ event for the Indian bond markets. Historically, the participation of foreign investors in the Indian markets has been tepid and virtually non-existent. The suggested inclusion could drive US$25 – 30 billion (~Rs 2.5 lakh Cr) over the next 18 months.

Markets have been a buzz on possible inclusions, the confirmation saw markets react positively across the yield curve with long bonds seeing heightened trading activity. The benchmark 10-year G-Sec stood at 7.10% at the time of writing this note.

Terms of the Inclusion

In a push for the global inclusion of Indian rupee bonds, the Indian government introduced the FAR (Fully Accessible Route) program in 2020 outlining a list of specified government securities. In addition, the government has undertaken substantive market reforms to aid foreign portfolio investments.

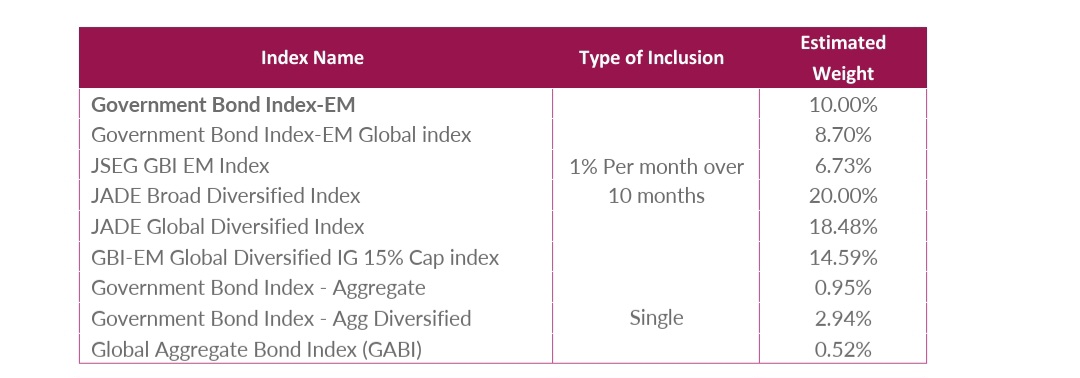

As per the index review, 23 bonds meet the Index eligibility criteria, with a combined notional value of approximately Rs 2.7 lakh Cr/ US$ 330 billion. As a result, India’s weight is expected to reach the maximum weight threshold of 10% in the GBI-EM GD, and approximately 8.7% in the GBI-EM Global index. As per the inclusion policy, India will enter the indices in June 2024 and the weight will be assigned gradually over a 10-month period through March 2025.

Apart from these indices, India is expected to enter a host of other indices including the global aggregate series, JADE series and JSEG GBI-EM index series of JP Morgan indices.

Source: JP Morgan, Axis MF Research. Data as of 31st August 2023

Implications for India

Passive trackers of the above indices hover at around US$250 billion. The staggered approach implies an inflow of US$ 1.5 – 2 billion per month in the 23 identified bonds. This flow is likely to boost India’s profile on the world stage and further strengthen local fundamentals. We believe the RBI could conduct sterilization operations during this inclusion period buffeting Forex reserves and the currency.

Based on this success, the government could notify additional bond series opening avenues for long-term debt capital to fund India’s vast infrastructure and development needs. By virtue of these bonds being rupee-denominated, we anticipate limited currency-related risks.

Market View

The news is a long-standing win for India’s policymakers and markets have rightfully cheered the announcement. Despite the negativity around global bond yields, we believe our markets will remain quite resilient after this inclusion. In the medium term, our target for the benchmark 10-year bond yields at 6.75% remains on track.

For the medium term, once this entire noise around Fed hikes and global yields stabilizes, we believe peak market rates are behind us and market yields could gradually soften. From a demand perspective, markets could see incremental buying from active foreign funds. That would probably be less than $ 5 billion before the index inclusion.

We have been macro-bullish on the perspective that it’s very difficult for the RBI to hike because inflation is going to be on the lower side. The only spoiler has been global yields and oil. Global yields are near its peak, and we don’t expect the Fed to hike rates further.

Oil prices remain a wildcard. With Crude prices spiking to US$95, markets are likely to bake in some degree of pessimism into the Indian bond markets. However, the two aspects could negate each other over the medium term. Finally, the inclusion by JP Morgan could be a precursor for other global index providers to add domestic bonds to global indices, amplifying the impact of flows. And hence the positive bond story is likely to continue for a while.

Strategy Call – Add duration

From a strategy perspective, we have added duration across portfolios within the respective investment mandates. The call was more from a macro perspective, not in the context to this inclusion news. We expect our duration call to add value in the medium term.

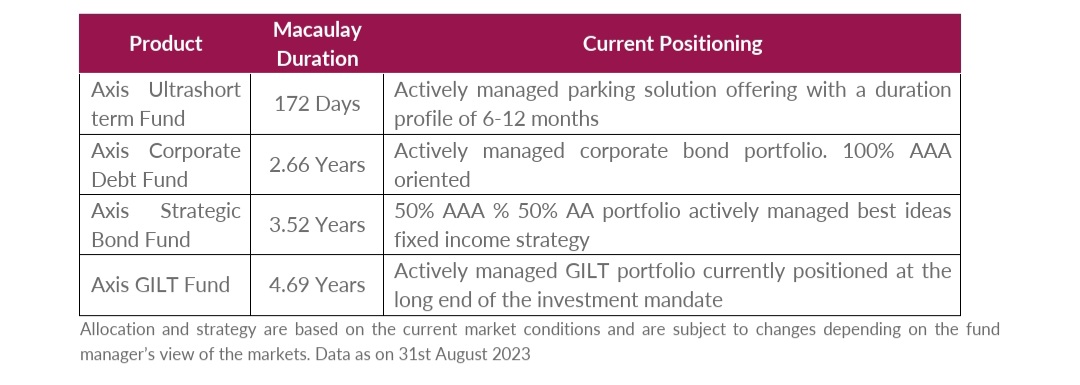

Investors could use this opportunity to top up on duration products with a structural allocation to short and medium duration funds and a tactical play on GILT funds.

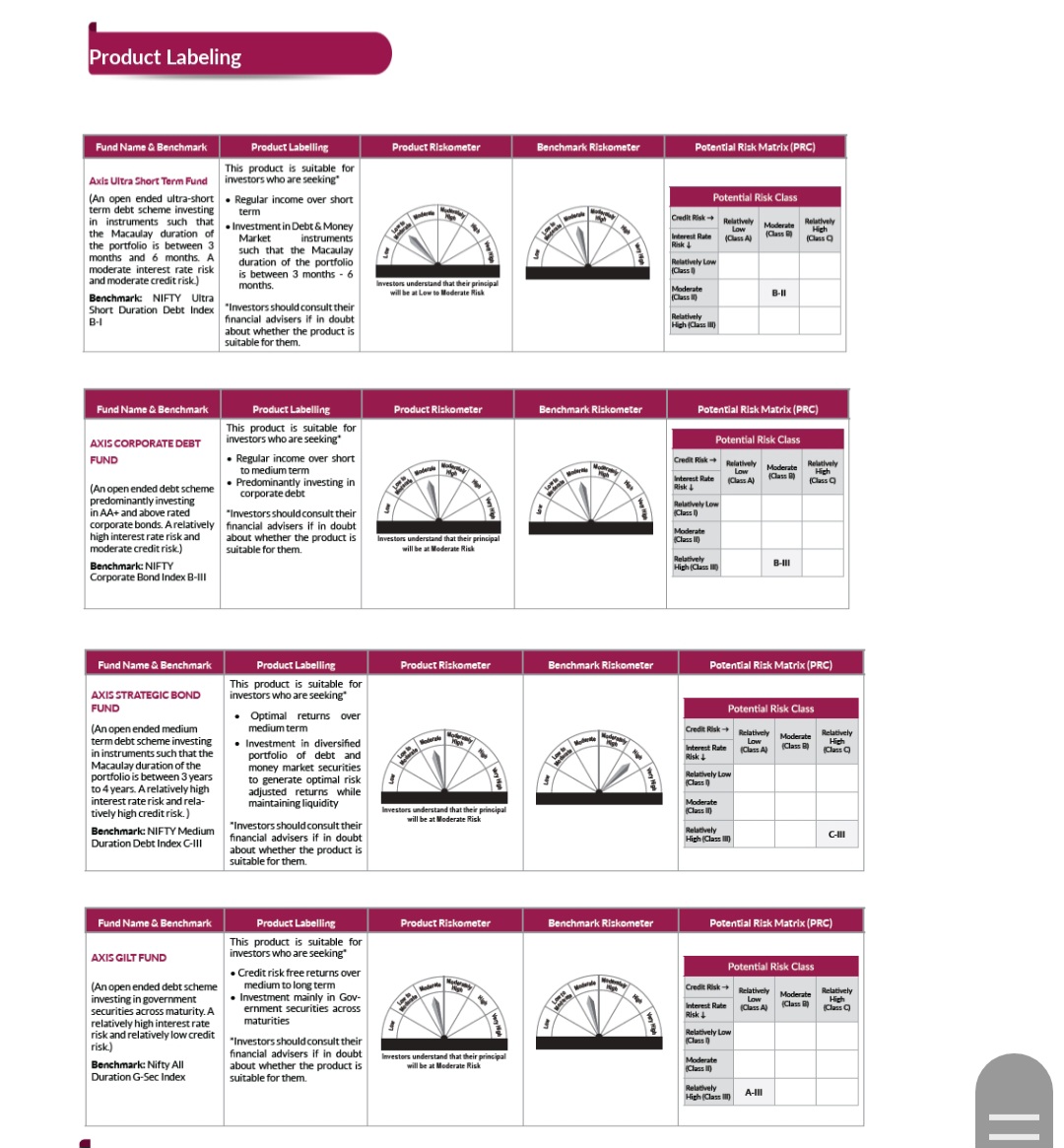

Funds in Focus